Specify Gradient for HMC Sampler

This example shows how to set up a Bayesian linear regression model for efficient posterior sampling using the Hamiltonian Monte Carlo (HMC) sampler. The prior distribution of the coefficients is a multivariate t, and the disturbance variance has an inverse gamma prior.

Consider the multiple linear regression model that predicts U.S. real gross national product (GNPR) using a linear combination of industrial production index (IPI), total employment (E), and real wages (WR).

For all  ,

,  is a series of independent Gaussian disturbances with a mean of 0 and variance

is a series of independent Gaussian disturbances with a mean of 0 and variance  . Assume these prior distributions.

. Assume these prior distributions.

is a 4-D t distribution with 30 degrees of freedom for each component, correlation matrix

is a 4-D t distribution with 30 degrees of freedom for each component, correlation matrix C, locationct, and scalest.

, with shape

, with shape  and scale

and scale  .

.

bayeslm treats these assumptions and the data likelihood as if the corresponding posterior is analytically intractable.

Declare a MATLAB® function that:

Accepts values of

and together in a column vector, and accepts values of the hyperparameters.

and together in a column vector, and accepts values of the hyperparameters.Returns the log of the joint prior distribution,

, given the values of and , and returns the gradient of the log prior density with respect to and

, given the values of and , and returns the gradient of the log prior density with respect to and  .

.

function [logPDF,gradient] = priorMVTIGHMC(params,ct,st,dof,C,a,b) %priorMVTIGHMC Log density of multivariate t times inverse gamma and %gradient % priorMVTIGHMC passes params(1:end-1) to the multivariate t density % function with dof degrees of freedom for each component and positive % definite correlation matrix C, and passes params(end) to the inverse % gamma distribution with shape a and scale b. priorMVTIG returns the % log of the product of the two evaluated densities and its gradient. % After applying the log, terms involving constants only are dropped from % logPDF. % % params: Parameter values at which the densities are evaluated, an % m-by-1 numeric vector. % % ct: Multivariate t distribution component centers, an (m-1)-by-1 % numeric vector. Elements correspond to the first m-1 elements % of params. % % st: Multivariate t distribution component scales, an (m-1)-by-1 % numeric vector. Elements correspond to the first m-1 elements % of params. % % dof: Degrees of freedom for the multivariate t distribution, a % numeric scalar or (m-1)-by-1 numeric vector. priorMVTIG expands % scalars such that dof = dof*ones(m-1,1). Elements of dof % correspond to the elements of params(1:end-1). % % C: correlation matrix for the multivariate t distribution, an % (m-1)-by-(m-1) symmetric, positive definite matrix. Rows and % columns correspond to the elements of params(1:end-1). % % a: Inverse gamma shape parameter, a positive numeric scalar. % % b: Inverse gamma scale parameter, a positive scalar. % beta = params(1:(end-1)); numCoeffs = numel(beta); sigma2 = params(end); tVal = (beta - ct)./st; expo = -(dof + numCoeffs)/2; logmvtDensity = expo*log(1 + (1/dof)*((tVal'/C)*tVal)); logigDensity = (-a - 1)*log(sigma2) - 1/(sigma2*b); logPDF = logmvtDensity + logigDensity; grad_beta = (expo/(1 + (1/dof)*(tVal'/C*tVal)))*((2/dof)*((tVal'/C)'./st)); grad_sigma = (-a - 1)/sigma2 + 1/(sigma2^2*b); gradient = [grad_beta; grad_sigma]; end

Create an anonymous function that operates like priorMVTIGHMC, but accepts the parameter values only and holds the hyperparameter values fixed at arbitrarily chosen values.

rng(1); % For reproducibility

dof = 30;

V = rand(4,4);

Sigma = V'*V;

st = sqrt(diag(Sigma));

C = Sigma./(st*st');

ct = -10*rand(4,1);

a = 10*rand;

b = 10*rand;

logPDF = @(params)priorMVTIGHMC(params,ct,st,dof,C,a,b);

Create a custom joint prior model for the linear regression parameters. Specify the number of predictors, p. Also, specify the function handle for priorMVTIGHMC and the variable names.

p = 3; PriorMdl = bayeslm(p,'ModelType','custom','LogPDF',logPDF,... 'VarNames',["IPI" "E" "WR"]);

PriorMdl is a customblm Bayesian linear regression model object representing the prior distribution of the regression coefficients and disturbance variance.

Load the Nelson-Plosser data set. Create variables for the response and predictor series. For numerical stability, convert the series to returns.

load Data_NelsonPlosser X = price2ret(DataTable{:,PriorMdl.VarNames(2:end)}); y = price2ret(DataTable{:,'GNPR'});

Estimate the marginal posterior distributions of and using the HMC sampler. To monitor the progress of the sampler, specify a verbosity level of 2. For numerical stability, specify reparameterization of the disturbance variance.

options = sampleroptions('Sampler','hmc','VerbosityLevel',2) PosteriorMdl = estimate(PriorMdl,X,y,'Options',options,'Reparameterize',true);

options =

struct with fields:

Sampler: 'HMC'

StepSizeTuningMethod: 'dual-averaging'

MassVectorTuningMethod: 'iterative-sampling'

NumStepSizeTuningIterations: 100

TargetAcceptanceRatio: 0.6500

NumStepsLimit: 2000

VerbosityLevel: 2

NumPrint: 100

o Tuning mass vector using method: iterative-sampling

o Initial step size for dual-averaging = 0.0625

|==================================================================================|

| ITER | LOG PDF | STEP SIZE | NUM STEPS | ACC RATIO | DIVERGENT |

|==================================================================================|

| 100 | 4.084850e+01 | 9.102e-02 | 55 | 6.300e-01 | 2 |

Finished mass vector tuning iteration 1 of 5.

o Initial step size for dual-averaging = 0.5

|==================================================================================|

| ITER | LOG PDF | STEP SIZE | NUM STEPS | ACC RATIO | DIVERGENT |

|==================================================================================|

| 100 | 4.222442e+01 | 5.154e-01 | 10 | 6.500e-01 | 0 |

|==================================================================================|

| ITER | LOG PDF | STEP SIZE | NUM STEPS | ACC RATIO | DIVERGENT |

|==================================================================================|

| 100 | 4.078962e+01 | 3.725e-02 | 6 | 8.000e-01 | 0 |

Finished mass vector tuning iteration 2 of 5.

o Initial step size for dual-averaging = 0.5

|==================================================================================|

| ITER | LOG PDF | STEP SIZE | NUM STEPS | ACC RATIO | DIVERGENT |

|==================================================================================|

| 100 | 3.676157e+01 | 2.791e-01 | 18 | 6.300e-01 | 0 |

|==================================================================================|

| ITER | LOG PDF | STEP SIZE | NUM STEPS | ACC RATIO | DIVERGENT |

|==================================================================================|

| 100 | 3.826446e+01 | 2.512e-01 | 4 | 7.950e-01 | 0 |

| 200 | 4.089424e+01 | 1.031e-01 | 16 | 8.567e-01 | 0 |

Finished mass vector tuning iteration 3 of 5.

o Initial step size for dual-averaging = 0.25

|==================================================================================|

| ITER | LOG PDF | STEP SIZE | NUM STEPS | ACC RATIO | DIVERGENT |

|==================================================================================|

| 100 | 4.256806e+01 | 3.299e-01 | 15 | 6.500e-01 | 0 |

|==================================================================================|

| ITER | LOG PDF | STEP SIZE | NUM STEPS | ACC RATIO | DIVERGENT |

|==================================================================================|

| 100 | 4.268094e+01 | 1.663e-02 | 2 | 7.900e-01 | 0 |

| 200 | 3.925843e+01 | 2.969e-01 | 15 | 8.500e-01 | 0 |

Finished mass vector tuning iteration 4 of 5.

o Initial step size for dual-averaging = 0.25

|==================================================================================|

| ITER | LOG PDF | STEP SIZE | NUM STEPS | ACC RATIO | DIVERGENT |

|==================================================================================|

| 100 | 4.294744e+01 | 3.210e-01 | 16 | 6.200e-01 | 0 |

|==================================================================================|

| ITER | LOG PDF | STEP SIZE | NUM STEPS | ACC RATIO | DIVERGENT |

|==================================================================================|

| 100 | 4.041877e+01 | 9.263e-02 | 4 | 7.750e-01 | 0 |

| 200 | 4.199693e+01 | 2.889e-01 | 5 | 8.400e-01 | 0 |

Finished mass vector tuning iteration 5 of 5.

o Tuning step size using method: dual-averaging. Target acceptance ratio = 0.65

o Initial step size for dual-averaging = 0.5

|==================================================================================|

| ITER | LOG PDF | STEP SIZE | NUM STEPS | ACC RATIO | DIVERGENT |

|==================================================================================|

| 100 | 4.219634e+01 | 3.394e-01 | 15 | 6.400e-01 | 0 |

Method: MCMC sampling with 10000 draws

Number of observations: 61

Number of predictors: 4

| Mean Std CI95 Positive Distribution

-----------------------------------------------------------------------

Intercept | 0.0076 0.0087 [-0.009, 0.024] 0.806 Empirical

IPI | -0.1638 0.1453 [-0.469, 0.101] 0.122 Empirical

E | 2.3732 0.5434 [ 1.401, 3.532] 1.000 Empirical

WR | -0.2315 0.3020 [-0.838, 0.348] 0.218 Empirical

Sigma2 | 0.0036 0.0007 [ 0.002, 0.005] 1.000 Empirical

PosteriorMdl is an empiricalblm model object storing the draws from the posterior distributions.

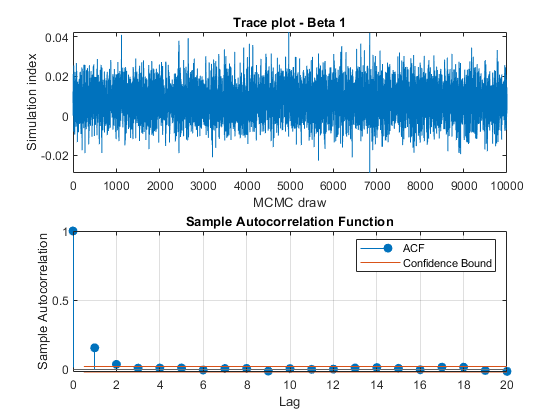

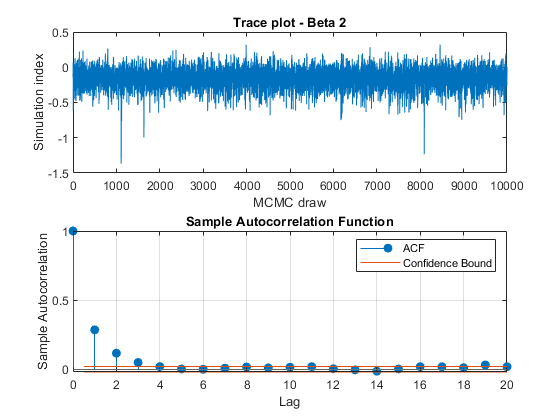

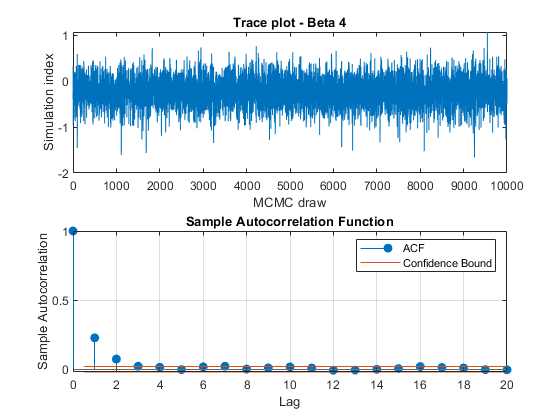

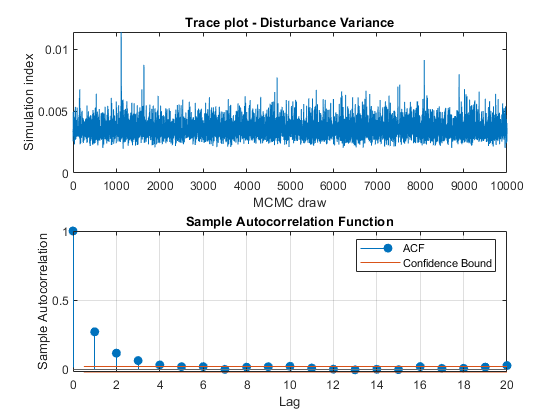

View trace plots and autocorrelation function (ACF) plots of the draws from the posteriors.

for j = 1:4 figure; subplot(2,1,1) plot(PosteriorMdl.BetaDraws(j,:)); title(sprintf('Trace plot - Beta %d',j)); xlabel('MCMC draw') ylabel('Simulation index') subplot(2,1,2) autocorr(PosteriorMdl.BetaDraws(j,:)) end figure; subplot(2,1,1) plot(PosteriorMdl.Sigma2Draws); title('Trace plot - Disturbance Variance'); xlabel('MCMC draw') ylabel('Simulation index') subplot(2,1,2) autocorr(PosteriorMdl.Sigma2Draws)

The trace plots show adequate mixing and no transient behavior. The autocorrelation plots show low correlation among subsequent samples.