Multivariate Models

Multivariate time series analysis is an extension of univariate time series analysis to a system of response variables for studying their dynamic relationship. To investigate the interactions and comovements of the response series, you can include lags of all response variables in each equation in the system.

To begin a multivariate time series analysis, test your response series for cointegration. If the response series do not exhibit cointegration, create a vector autoregression (VAR) model for the series. Econometrics Toolbox™ supports frequentist and Bayesian VAR analysis tools. If the response series exhibit cointegration, create a vector error-correction (VEC) model for the series. For more details, see Vector Autoregression (VAR) Models.

Categories

- Cointegration Analysis

Engle-Granger cointegration test, and Johansen cointegration and constraint tests

- Vector Autoregression Models

Stationary multivariate linear models including exogenous predictor variables

- Vector Error-Correction Models

Multivariate linear models including cointegrating relations and exogenous predictor variables

- Bayesian Vector Autoregression Models

Posterior estimation and simulation using a variety of prior models for VARX model coefficients and innovations covariance matrix

Featured Examples

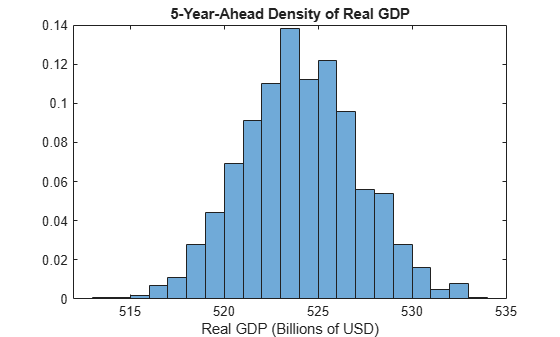

Model the United States Economy

Use a vector error-correction model as a linear alternative to the Smets-Wouters DSGE macroeconomic model.

Incorporate Macroeconomic Scenario Projections in Loan Portfolio ECL Calculations

Generate macroeconomic scenarios and perform expected credit loss (ECL) calculations for a portfolio of loans.