estimate

Syntax

Description

EstMdl = estimate(Mdl,tt0,Y)Mdl. estimate fits the model to the response

data Y, and initializes the estimation procedure by treating the

parameter values of the fully specified threshold transitions tt0 as

initial values. estimate implements a version of the conditional

least-squares algorithm described in [4].

Examples

Assess estimation accuracy using simulated data from a known data-generating process (DGP). This example uses arbitrary parameter values.

Create Model for DGP

Create a discrete threshold transition at mid-level 1.

ttDGP = threshold(1)

ttDGP =

threshold with properties:

Type: 'discrete'

Levels: 1

Rates: []

StateNames: ["1" "2"]

NumStates: 2

ttDGP is a threshold object representing the state-switching mechanism of the DGP.

Create the following fully specified self-exciting TAR (SETAR) model for the DGP.

State 1: .

State 2: .

.

Specify the submodels by using arima.

mdl1DGP = arima(Constant=0); mdl2DGP = arima(Constant=2); mdlDGP = [mdl1DGP mdl2DGP];

Because the innovations distribution is invariant across states, the tsVAR software ignores the value of the submodel innovations variance (Variance property).

Create a threshold-switching model for the DGP. Specify the model-wide innovations variance.

MdlDGP = tsVAR(ttDGP,mdlDGP,Covariance=1);

MdlDGP is a tsVAR object representing the DGP.

Simulate Response Paths from DGP

Generate a random response path of length 100 from the DGP. By default, simulate assumes a SETAR model with delay . In other words, the threshold variable is .

rng(1) % For reproducibiliy

y = simulate(MdlDGP,100);y is a 100-by-1 vector of representing the simulated response path.

Create Model for Estimation

Create a partially specified threshold-switching model that has the same structure as the data-generating process, but specify the transition mid-level, submodel coefficients, and model-wide constant as unknown for estimation.

tt = threshold(NaN); mdl1 = arima('Constant',NaN); mdl2 = arima('Constant',NaN); Mdl = tsVAR(tt,[mdl1,mdl2],'Covariance',NaN);

Mdl is a partially specified tsVAR object representing a template for estimation. NaN-valued elements of the Switch and Submodels properties indicate estimable parameters.

Mdl is agnostic of the threshold variable; tsVAR object functions enable you to specify threshold variable characteristics or data.

Create Threshold Transitions Containing Initial Values

The estimation procedure requires initial values for all estimable threshold transition parameters.

Fully specify a threshold transition that has the same structure as tt, but set the mid-level to 0.

tt0 = threshold(0);

tt0 is a fully specified threshold object.

Estimate Model

Fit the model to the simulated path. By default, the model is self-exciting and the delay of the threshold variable is .

EstMdl = estimate(Mdl,tt0,y)

EstMdl =

tsVAR with properties:

Switch: [1×1 threshold]

Submodels: [2×1 varm]

NumStates: 2

NumSeries: 1

StateNames: ["1" "2"]

SeriesNames: "1"

Covariance: 1.0225

EstMdl is a fully specified tsVAR object representing the estimated SETAR model.

Display an estimation summary of the submodels.

summarize(EstMdl)

Description

1-Dimensional tsVAR Model with 2 Submodels

Switch

Transition Type: discrete

Estimated Levels: 1.128

Fit

Effective Sample Size: 99

Number of Estimated Parameters: 2

Number of Constrained Parameters: 0

LogLikelihood: -141.574

AIC: 287.149

BIC: 292.339

Submodels

Estimate StandardError TStatistic PValue

________ _____________ __________ __________

State 1 Constant(1) -0.12774 0.13241 -0.96474 0.33467

State 2 Constant(1) 2.1774 0.16829 12.939 2.7264e-38

The estimates are close to their true values.

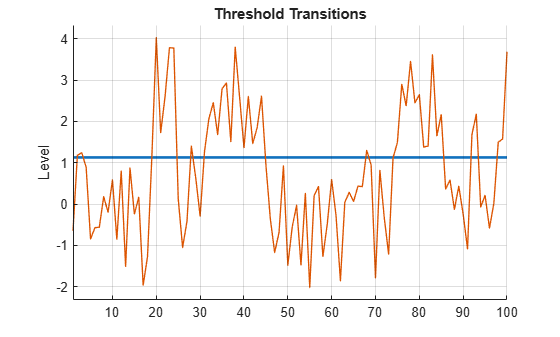

Plot the estimated switching mechanism with the threshold data, which is the response data.

figure

ttplot(EstMdl.Switch,'Data',y)

estimate does not fit the delay parameter to the data; you must specify its value when you call estimate. This example shows how to tune .

Create the following fully specified SETAR model for the DGP.

State 1: , where .

State 2: , where .

The system is in state 1 when , and it is in state 2 otherwise.

ttDGP = threshold(0); mdl1DGP = arima(Constant=0,Variance=1); mdl2DGP = arima(Constant=2,Variance=2); mdlDGP = [mdl1DGP; mdl2DGP]; MdlDGP = tsVAR(ttDGP,mdlDGP);

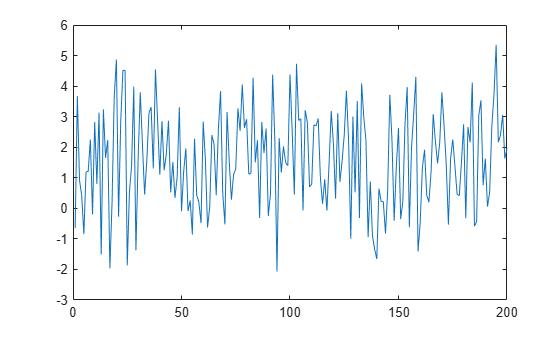

Generate a random response path of length 200 from the DGP. Specify that the threshold variable delay is 4.

rng(1) % For reproducibiliy

y = simulate(MdlDGP,200,Delay=4);

plot(y)

Create a partially specified threshold-switching model that has the same structure as the data-generating process, but specify the transition mid-level, submodel coefficients, and state-specific variances as unknown for estimation.

tt = threshold(NaN); mdl = arima(0,0,0); Mdl = tsVAR(tt,[mdl; mdl]);

Fully specify a threshold transition that has the same structure as tt, but set the mid-level to 0.5.

tt0 = threshold(0.5);

Tune by choosing a set of plausible values for it, and by fitting the SETAR model to the simulated data for each value in the set. Choose the model that maximizes the loglikelihood.

d = 1:8; nd = numel(d); logL = zeros(nd,1); % Preallocate for loglikelihoods EstMdl = cell(nd,1); % Preallocate for estimated models for j = 1:nd [EstMdl{j},logL(j)] = estimate(Mdl,tt0,y,Delay=d(j)); end

Extract the model that maximizes the loglikelihood.

[~,optDelay] = max(logL)

optDelay = 4

OptEstMdl = EstMdl{optDelay};The optimal delay is 4, which matches the delay of the DGP.

Display an estimation summary of the optimal model, and display its estimated switching mechanism.

summarize(OptEstMdl)

Description

1-Dimensional tsVAR Model with 2 Submodels

Switch

Transition Type: discrete

Estimated Levels: -0.063

Fit

Effective Sample Size: 196

Number of Estimated Parameters: 2

Number of Constrained Parameters: 0

LogLikelihood: -336.184

AIC: 676.367

BIC: 682.923

Submodels

Estimate StandardError TStatistic PValue

________ _____________ __________ __________

State 1 Constant(1) -0.33535 0.24271 -1.3817 0.16707

State 2 Constant(1) 2.0073 0.10647 18.853 2.7794e-79

The estimates are close to the parameters of the DGP.

Create the following fully specified SETAR model for the DGP.

State 1: .

State 2: .

State 3:.

.

The system is in state 1 when , the system is in state 2 when 3, and the system is in state 3 otherwise.

t = [-3 3];

ttDGP = threshold(t);

constant1 = [-1; -4];

constant2 = [1; 4];

constant3 = [1; 4];

AR1 = [-0.5 0.1; 0.2 -0.75];

AR3 = [0.5 0.1; 0.2 0.75];

Sigma = [2 -1; -1 1];

mdl1DGP = varm(Constant=constant1,AR={AR1});

mdl2DGP = varm(Constant=constant2);

mdl3DGP = varm(Constant=constant3,AR={AR3});

mdlDGP = [mdl1DGP; mdl2DGP; mdl3DGP];

MdlDGP = tsVAR(ttDGP,mdlDGP,Covariance=Sigma);Generate a random response path of length 1000 from the DGP. Specify that second response variable with a delay of 4 as the threshold variable.

rng(10) % For reproducibiliy

y = simulate(MdlDGP,1000,Index=2,Delay=4);Create a partially specified threshold-switching model that has the same structure as the DGP, but specify the transition mid-level, submodel coefficients, and model-wide covariance as unknown for estimation.

tt = threshold([NaN; NaN]); mdlar = varm(2,1); mdlc = varm(2,0); Mdl = tsVAR(tt,[mdlar; mdlc; mdlar],Covariance=nan(2));

Fully specify a threshold transition that has the same structure as tt, but set the mid-levels to -1 and 1.

t0 = [-1 1]; tt0 = threshold(t0);

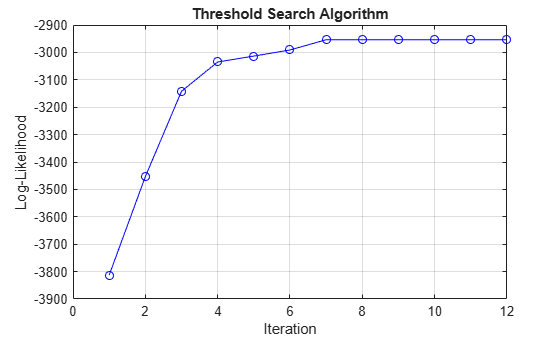

Fit the threshold-switching model to the simulated series. Specify the threshold variable . Plot the loglikelihood after each iteration of the threshold search algorithm.

EstMdl = estimate(Mdl,tt0,y,IterationPlot=true,Index=2,Delay=4);

The plot displays the evolution of the loglikelihood as the estimation procedure searches for optimal levels. The procedure terminates when one of the stopping criteria is satisfied.

Display an estimation summary of the model.

summarize(EstMdl)

Description

2-Dimensional tsVAR Model with 3 Submodels

Switch

Transition Type: discrete

Estimated Levels: -2.882 3.003

Fit

Effective Sample Size: 996

Number of Estimated Parameters: 14

Number of Constrained Parameters: 0

LogLikelihood: -2953.685

AIC: 5935.369

BIC: 6004.022

Submodels

Estimate StandardError TStatistic PValue

________ _____________ __________ __________

State 1 Constant(1) -1.0327 0.098764 -10.457 1.3658e-25

State 1 Constant(2) -3.9522 0.07149 -55.283 0

State 1 AR{1}(1,1) -0.46607 0.043573 -10.696 1.0602e-26

State 1 AR{1}(2,1) 0.17945 0.03154 5.6895 1.2742e-08

State 1 AR{1}(1,2) 0.08709 0.016751 5.1992 2.0015e-07

State 1 AR{1}(2,2) -0.75546 0.012125 -62.307 0

State 2 Constant(1) 0.95354 0.10428 9.1441 6.0145e-20

State 2 Constant(2) 4.131 0.075482 54.728 0

State 3 Constant(1) 1.1151 0.067611 16.494 4.0849e-61

State 3 Constant(2) 3.8837 0.048939 79.357 0

State 3 AR{1}(1,1) 0.53183 0.040671 13.077 4.486e-39

State 3 AR{1}(2,1) 0.19554 0.029439 6.642 3.094e-11

State 3 AR{1}(1,2) 0.097517 0.012623 7.7254 1.1149e-14

State 3 AR{1}(2,2) 0.75156 0.0091369 82.255 0

Consider a smooth threshold-switching (STAR) model for the real US GDP growth rate, where each submodel is AR(4) and the threshold variable is the unemployment growth rate.

Create a partially specified threshold transition for the unemployment growth rate. Specify the normal cdf transition function, and an unknown, estimable mid-level and rate. Label the states "Contraction" and "Expansion".

tt = threshold(NaN,Type="normal",Rates=NaN, ... StateNames=["Contraction" "Expansion"]);

tt is a partially specified threshold object, and it is agnostic of the variable and data it represents.

Create a threshold-switching model for the real US GDP growth rate. Label the series "rRGDP".

mdl = arima(4,0,0);

submdls = [mdl; mdl];

Mdl = tsVAR(tt,submdls,SeriesNames="rRGDP");Load the quarterly US macroeconomic data set Data_USEconModel.mat. Compute the real GDP percent growth and unemployment growth.

load Data_USEconModel DataTimeTable = rmmissing(DataTimeTable,DataVariables=["GDP" "GDPDEF" "UNRATE"]); RGDP = DataTimeTable.GDP./DataTimeTable.GDPDEF; rRGDP = price2ret(RGDP)*100; % Response data gUNRATE = diff(DataTimeTable.UNRATE); % Exogenous threshold data dates = DataTimeTable.Time(2:end);

Suppose the estimation period includes growth rates from the first quarter of 1950. Identify the estimation period in the date base.

startEst = datetime(1950,1,1); idxEst = dates >= startEst;

To initialize the estimation procedure, fully specify a threshold transition that has the same structure as tt, but set the mid-level to -0.5 with a rate of 100.

tt0 = threshold(-0.5,Type=tt.Type,Rates=100,StateNames=tt.StateNames);

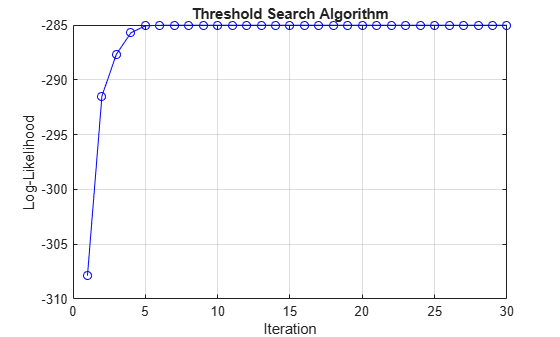

Fit the STAR model to the estimation period of the US GDP growth rate series. Specify the following parameters:

Set

Y0to the responses before the estimation period to initialize the AR submodel components.Set

Typeto "exogenous" to characterize the threshold variable.Set Z to the threshold variable data

gUNRATEin the estimation period.Set

MaxRateto150to expand the search for the optimal transition function rate.Plot the evolution of the loglikelihood.

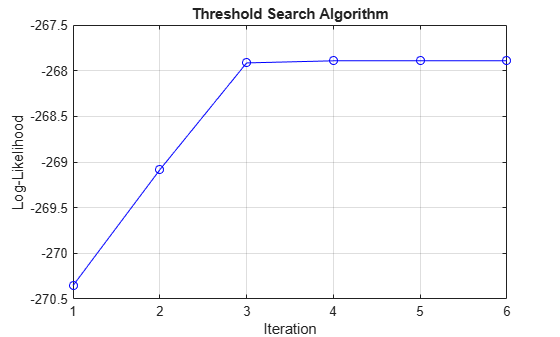

EstMdl = estimate(Mdl,tt0,rRGDP(idxEst),Y0=rRGDP(~idxEst), ... Z=gUNRATE(idxEst),Type="exogenous",MaxRate=150,IterationPlot=true);

Display an estimation summary and plot the estimated switching mechanism with the threshold data.

summarize(EstMdl)

Description

1-Dimensional tsVAR Model with 2 Submodels

Switch

Transition Type: normal

Estimated Levels: 0.208

Estimated Rates: 74.994

Fit

Effective Sample Size: 237

Number of Estimated Parameters: 10

Number of Constrained Parameters: 0

LogLikelihood: -285.022

AIC: 590.043

BIC: 624.724

Submodels

Estimate StandardError TStatistic PValue

_________ _____________ __________ __________

State 1 Constant(1) 1.0473 0.11549 9.068 1.2125e-19

State 1 AR{1}(1,1) 0.15792 0.068783 2.2959 0.021679

State 1 AR{2}(1,1) 0.059888 0.066409 0.9018 0.36716

State 1 AR{3}(1,1) -0.10455 0.070384 -1.4854 0.13744

State 1 AR{4}(1,1) -0.098037 0.063249 -1.55 0.12114

State 2 Constant(1) -0.12491 0.15383 -0.81197 0.41681

State 2 AR{1}(1,1) 0.15366 0.13993 1.0981 0.27215

State 2 AR{2}(1,1) -0.027925 0.16754 -0.16667 0.86763

State 2 AR{3}(1,1) -0.24366 0.12778 -1.9068 0.056543

State 2 AR{4}(1,1) -0.075389 0.14024 -0.53759 0.59086

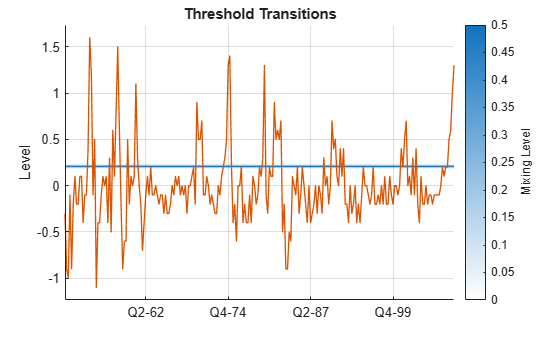

figure ttplot(EstMdl.Switch,Data=gUNRATE(idxEst)) dEst = dates(idxEst); xticklabels(string(dEst(xticks)))

The large rate suggests little mixing occurs between the models of each regime. When the quarterly unempoyment growth is less than 0.206%, the dominant model for the US GDP growth rate is in EstMdl.Submodels(1). Otherwise, the dominant submodel is in EstMdl.Submodels(2).

Many of the coefficients are insignificant, which can suggest a search for a simpler model.

This example shows how to specify equality constraints on estimable submodel coefficients and threshold parameters.

Consider the model for the real US GDP growth rate in Specify Presample Data for STAR Model Estimation. Assume the submodels are AR(4), but they include only the model constant (time trend in differenced series) and fourth lag. Also, suppose the transition function rate 3 for the unemployment growth series.

Create the partially specified threshold transition for the unemployment growth rate. Specify the known transition rate.

rConstraint = 3; tt = threshold(NaN,Type="normal",Rates=rConstraint, ... StateNames=["Contraction" "Expansion"]);

Create a threshold-switching model for the real US GDP growth rate. Explicitly specify the AR lags to include in the submodels by using the ARLags option.

mdl = arima(ARLags=4);

submdls = [mdl; mdl];

Mdl = tsVAR(tt,submdls,SeriesNames="rRGDP");Load the quarterly US macroeconomic data set Data_USEconModel.mat. Compute the real GDP percent growth and unemployment growth.

load Data_USEconModel DataTimeTable = rmmissing(DataTimeTable,DataVariables=["GDP" "GDPDEF" "UNRATE"]); RGDP = DataTimeTable.GDP./DataTimeTable.GDPDEF; rRGDP = price2ret(RGDP)*100; % Response data gUNRATE = diff(DataTimeTable.UNRATE); % Exogenous threshold data dates = DataTimeTable.Time(2:end);

Suppose the estimation period includes growth rates from the first quarter of 1950. Identify the estimation period in the date base.

startEst = datetime(1950,1,1); idxEst = dates >= startEst;

Fully specify a threshold transition that has the same structure as tt, including the equality constraint on the transition function rate. Set the initial mid-level to 0.

tt0 = threshold(0,Type=tt.Type,Rates=rConstraint,StateNames=tt.StateNames);

Fit the STAR model to the estimation period of the US GDP growth rate series. Specify the following parameters:

Set

Y0to the responses before the estimation period to initialize the AR submodel components.Set

Typeto"exogenous"to characterize the threshold variable.Set

Zto the threshold variable datagUNRATEin the estimation period.Set

MaxRateto 150 to expand the search for the optimal transition function rate.Plot the evolution of the loglikelihood.

EstMdl = estimate(Mdl,tt0,rRGDP(idxEst),Y0=rRGDP(~idxEst), ... Z=gUNRATE(idxEst),Type="exogenous",IterationPlot=true);

Display an estimation summary and plot the estimated switching mechanism with the threshold data.

summarize(EstMdl)

Description

1-Dimensional tsVAR Model with 2 Submodels

Switch

Transition Type: normal

Estimated Levels: 0.228

Estimated Rates: 3.000

Fit

Effective Sample Size: 237

Number of Estimated Parameters: 4

Number of Constrained Parameters: 6

LogLikelihood: -267.892

AIC: 543.784

BIC: 557.656

Submodels

Estimate StandardError TStatistic PValue

_________ _____________ __________ __________

State 1 Constant(1) 1.5928 0.087805 18.14 1.543e-73

State 1 AR{1}(1,1) 0 0 NaN NaN

State 1 AR{2}(1,1) 0 0 NaN NaN

State 1 AR{3}(1,1) 0 0 NaN NaN

State 1 AR{4}(1,1) -0.11789 0.067607 -1.7438 0.081194

State 2 Constant(1) -0.73667 0.15808 -4.6601 3.1609e-06

State 2 AR{1}(1,1) 0 0 NaN NaN

State 2 AR{2}(1,1) 0 0 NaN NaN

State 2 AR{3}(1,1) 0 0 NaN NaN

State 2 AR{4}(1,1) -0.040337 0.1299 -0.31053 0.75616

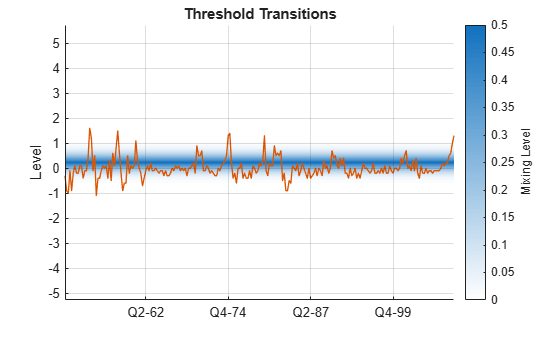

figure ttplot(EstMdl.Switch,Data=gUNRATE(idxEst)) dEst = dates(idxEst); xticklabels(string(dEst(xticks)))

Consider the following data-generating process (DGP) for a 2-D time-varying TAR (TVTAR) model containing an exogenous regression component.

State 1: , where and is the 2-by-2 identity matrix.

State 2: , where .

State 3: , where .

The exogenous threshold variable represents a linear time trend over the sample period. In this example, is the sampling period normalized by the sample size.

The system is in state 1 when , the system is in state 2 when , and the system is in state 3 otherwise.

Create a TVTAR model that represents the DGP.

tDGP = [0.3 0.6]; ttDGP = threshold(tDGP); % Constant vectors C1 = [1;-1]; C2 = [2;-2]; C3 = [3;-3]; % Common Autoregression coefficient AR = {[0.6 0.1; 0.4 0.2]}; % Regression coefficient vectors Beta1 = [0.2;-0.4]; Beta2 = [0.6;-1.0]; Beta3 = [0.9;-1.3]; % Innovations covariance matrices Sigma1 = 0.5*eye(2); Sigma2 = eye(2); Sigma3 = 1.5*eye(2); % VAR Submodels mdl1 = varm(Constant=C1,AR=AR,Beta=Beta1,Covariance=Sigma1); mdl2 = varm(Constant=C2,AR=AR,Beta=Beta2,Covariance=Sigma2); mdl3 = varm(Constant=C3,AR=AR,Beta=Beta3,Covariance=Sigma3); mdlDGP = [mdl1; mdl2; mdl3]; DGP = tsVAR(ttDGP,mdlDGP);

For the exogenous predictors , simulate a 2-D 1000-period path from the Gaussian distribution with mean 0 and standard deviation 10.

rng(1); % For reproducibility

numPeriods = 1000;

X = 10*randn(numPeriods,2);For the threshold variable, create a 1000-element vector of equally spaced elements from 0 to 1.

z = linspace(0,1,numPeriods)';

Simulate a 1000-period path from the DGP.

Y = simulate(DGP,numPeriods,X=X,Type="exogenous",Z=z);Create a TVTAR model template for estimation. Specify all estimable parameters as unknown by using NaNs.

t = [NaN NaN]; tt = threshold(t); mdl = varm(2,1); % Unknown contsant and AR coefficient by default mdl.Beta = NaN(2,1); % Configure exogenous regression component for estimation Mdl = tsVAR(tt,[mdl; mdl; mdl]);

Specify initial values of 0.25 and 0.7 for the regime thresholds.

t0 = [.25 .7]; tt0 = threshold(t0);

The largest lag among all models is 1. Therefore, the estimation procedure requires one presample observation to initialize the model.

Identify indices for the required presample, and identify indices for the estimation sample.

p = mdl.P; idxPre = 1:p; idxEst = (p + 1):numPeriods;

Fit the TVTAR model to the data. Specify presample responses Y0, characterize the threshold variable Type and provide its data Z, and specify the exogenous data X.

EstMdl = estimate(Mdl,tt0,Y(idxEst,:),Y0=Y(idxPre,:), ... Type="exogenous",Z=z(idxEst),X=X(idxEst,:));

Display an estimation summary separately for each state, and display the estimated threshold transitions.

summarize(EstMdl,1)

Description

2-Dimensional VAR Submodel, State 1

Submodel

Estimate StandardError TStatistic PValue

________ _____________ __________ ___________

State 1 Constant(1) 0.6284 0.1463 4.2952 1.7456e-05

State 1 Constant(2) -0.86147 0.1664 -5.1771 2.2538e-07

State 1 AR{1}(1,1) 0.64569 0.046378 13.922 4.6483e-44

State 1 AR{1}(2,1) 0.41777 0.052749 7.92 2.3751e-15

State 1 AR{1}(1,2) 0.11447 0.029747 3.8481 0.00011901

State 1 AR{1}(2,2) 0.18968 0.033833 5.6064 2.0657e-08

State 1 Beta(1,1) 0.12661 0.01005 12.598 2.1562e-36

State 1 Beta(2,1) -0.28306 0.01143 -24.765 2.1434e-135

summarize(EstMdl,2)

Description

2-Dimensional VAR Submodel, State 2

Submodel

Estimate StandardError TStatistic PValue

________ _____________ __________ __________

State 2 Constant(1) 2.0016 0.20741 9.6503 4.9028e-22

State 2 Constant(2) -1.919 0.2359 -8.1345 4.1377e-16

State 2 AR{1}(1,1) 0.59692 0.033401 17.871 1.9847e-71

State 2 AR{1}(2,1) 0.37274 0.03799 9.8117 1.0027e-22

State 2 AR{1}(1,2) 0.1173 0.023148 5.0674 4.0337e-07

State 2 AR{1}(2,2) 0.18002 0.026327 6.8376 8.0531e-12

State 2 Beta(1,1) 0.6689 0.014264 46.896 0

State 2 Beta(2,1) -1.122 0.016223 -69.16 0

summarize(EstMdl,3)

Description

2-Dimensional VAR Submodel, State 3

Submodel

Estimate StandardError TStatistic PValue

________ _____________ __________ ___________

State 3 Constant(1) 3.1135 0.10796 28.841 6.587e-183

State 3 Constant(2) -3.135 0.12279 -25.533 8.5621e-144

State 3 AR{1}(1,1) 0.61547 0.011379 54.089 0

State 3 AR{1}(2,1) 0.40065 0.012942 30.958 1.9802e-210

State 3 AR{1}(1,2) 0.10685 0.0089014 12.004 3.4042e-33

State 3 AR{1}(2,2) 0.19124 0.010124 18.889 1.3979e-79

State 3 Beta(1,1) 0.92011 0.0080742 113.96 0

State 3 Beta(2,1) -1.3378 0.0091834 -145.68 0

EstMdl.Switch

ans =

threshold with properties:

Type: 'discrete'

Levels: [0.3096 0.5887]

Rates: []

StateNames: ["1" "2" "3"]

NumStates: 3

Input Arguments

Name-Value Arguments

Output Arguments

Tips

Several factors can lead to poor estimates of model parameters. The factors include:

Threshold data does not cross levels or sufficiently sample submodels.

Mdlcontains more estimable parameters than the sample size supports.High-rate transitions are indistinguishable.

Self-exciting autoregressive models have multiple sources of endogenous dynamics.

To improve estimates, perform these actions:

Control the parameter search by experimenting with the

'MaxLevel'and'MaxRate'name-value arguments.Consider a parsimonious model with initial levels within the range of threshold variable data.

Constrain specific parameters to potentially improve performance.

To estimate the delay d in a self-exciting model, compare the loglikelihood

logLwith different specifications for the'Delay'name-value argument. In practice, usually d is limited to a range of reasonable values.You can estimate a simple time-varying STAR (TVSTAR) model by specifying exogenous threshold data z = t, which is a linear time trend over the sample period [3].

Algorithms

estimatesearches over levels and rates forEstMdl.Switchwhile solving a conditional least-squares problem for submodel parameters, maximizing the data likelihood, as described in [4].logLis conditional on the optimal parameter values inEstMdl.Switch.Models with smooth transitions (STAR models) represent the response as a weighted mixture of conditional means from all submodels ([4], Eqn. 3.6).

estimatedetermines the weights by the value of the threshold variable, z or yj,t−d, relative to threshold levels.estimatetreats models with discrete transitions (TAR models) as logistic STAR models with transition rates set to'MaxRate'in order to disambiguate search levels that fall between threshold variable data.estimatehandles two types of equality constraints.estimatecomputes innovations variances and covariances after estimation. Therefore, you cannot constrain them.

References

[2] Hamilton, James D. Time Series Analysis. Princeton, NJ: Princeton University Press, 1994.

Version History

Introduced in R2021b