setConditionalBudget

Description

obj = setConditionalBudget(obj,ConditionalBudgetThreshold,ConditionalUpperBudget)Portfolio,

PortfolioCVaR, or PortfolioMAD

objects. If the weight of an asset exceeds the

ConditionalBudgetThreshold value, the weight of that

asset is added to the aggregate sum that is bound by the

ConditionalUpperBudget value. For more information, see

Conditional Budget Constraints .

This constraint supports the Undertakings for Collective Investment in Transferable Securities (UCITS) Directive. The UCITS asset regulation states that any investments in excess of 5% must not exceed 40% of the total portfolio. This constraint is a conditional budget constraint. For more information, see Undertakings for Collective Investment in Transferable Securities and Adding Constraints to Satisfy UCITS Directive.

For details on the respective workflows when using these different objects, see Portfolio Object Workflow, PortfolioCVaR Object Workflow, and PortfolioMAD Object Workflow.

Examples

This example shows the workflow to add a conditional budget constraint for a portfolio optimization problem. The conditional budget constraint enforces a limit on the total proportion that you can invest in assets that pass a prescribed threshold.

In mathematical terms, the conditional budget constraint has the following form:

where and represents the asset weights.

Create Portfolio Object

To solve a portfolio problem with this constraint, start by creating a Portfolio object with default constraints. In addition to using a Portfolio object, you can also perform this workflow using a PortfolioCVaR or PortfolioMAD object.

% Load data load CAPMuniverse.mat tol = 1e-8; p = Portfolio('AssetList',Assets(1:12)); p = estimateAssetMoments(p,Data(:,1:12));

Using setConditionalBudget, set a conditional budget constraint that limits the aggregate weight that can be invested in assets that exceed 10% to 50%.

% Assets with weights above 10% must not exceed 50% of the total portfolio

p = setConditionalBudget(p,0.1,0.5);At this point, the portfolio problem is unbounded and computing any optimal portfolio results in an error. Use setBounds to add bounds to the portfolio weights.

% Weights must be between -1 and 1

p = setBounds(p,-1,1);Compute Efficient Frontier

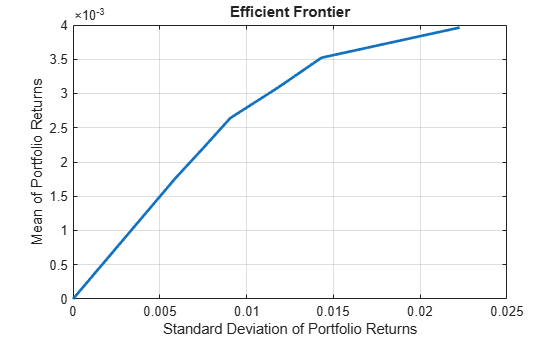

The most common workflow is to estimate a set of portfolios on the efficient frontier. The efficient frontier is the curve that shows the tradeoff between the return and risk achieved by Pareto-optimal portfolios. For a given return level, the portfolio on the efficient frontier is the one that minimizes the risk while maintaining the desired return. Conversely, for a given risk level, the portfolio on the efficient frontier is the one that maximizes return while maintaining the desired risk level.

% Compute efficient frontier

w = estimateFrontier(p)w = 12×10

0.0000 0.0368 0.0737 0.1105 0.1473 0.1979 0.2408 0.2686 0.5000 0.5000

0.0000 0.0008 0.0016 0.0023 0.0031 0.0082 0.0108 0.0762 0.0317 0.1000

0.0000 -0.0222 -0.0444 -0.0665 -0.0887 -0.1084 -0.1294 -0.2283 -0.2164 -1.0000

-0.0000 -0.0218 -0.0436 -0.0654 -0.0871 -0.1144 -0.1386 -0.4499 -0.4361 -1.0000

0.0000 -0.0087 -0.0175 -0.0262 -0.0350 -0.0448 -0.0539 -0.0260 -0.0300 0.1000

-0.0000 0.0398 0.0796 0.1194 0.1592 0.2122 0.2578 0.2314 0.1000 0.1000

0.0000 0.0366 0.0732 0.1098 0.1464 0.1000 0.1000 0.1000 0.1000 0.1000

-0.0000 -0.0282 -0.0565 -0.0847 -0.1129 -0.1424 -0.1712 -0.1291 -0.2717 0.1000

0.0000 0.0060 0.0120 0.0180 0.0240 0.0506 0.0658 0.1000 0.1000 0.1000

-0.0000 0.0111 0.0222 0.0333 0.0444 0.0746 0.0941 0.1000 0.1000 0.1000

0.0000 0.0131 0.0263 0.0394 0.0526 0.0706 0.0859 0.1000 0.1000 0.1000

0.0000 -0.0127 -0.0254 -0.0381 -0.0508 -0.0707 -0.0866 0.1000 0.1000 0.1000

plotFrontier(p,w)

Check that none of the assets that exceed 10% go above 50%.

% Keep weights above 10% threshold

auxW = w;

auxW(w <= 0.1 + tol) = 0;

conditionalBudget = sum(auxW)conditionalBudget = 1×10

0 0 0 0.3397 0.4529 0.4101 0.4986 0.5000 0.5000 0.5000

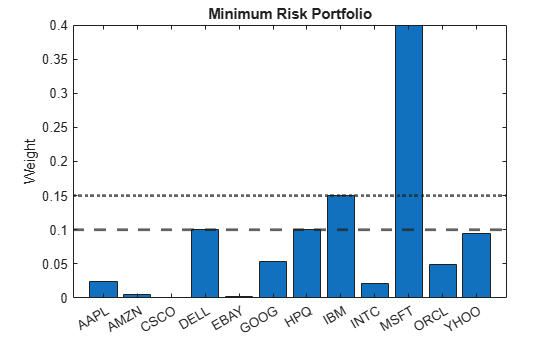

This example shows how to set a different conditional budget threshold for one of the assets in the portfolio. setConditionalBudget supports a vector input for the CondtionalBudgetThreshold argument, where each entry represents the conditional threshold for each asset. In this example, assume that the conditional budget threshold for all assets is 10% except for IBM. The conditional budget threshold for IBM is 15%.

To solve a portfolio problem with this constraint, start by creating a PortfolioCVaR object with default constraints. In addition to using a PortfolioCVaR object, you can also perform this workflow using a Portfolio or PortfolioMAD object.

% Load data load CAPMuniverse.mat tol = 1e-8; startRow = find(~isnan(Data(:,6)),1); p = PortfolioCVaR(AssetList=Assets(1:12), ... AssetScenarios=Data(startRow:end,1:12),ProbabilityLevel=0.95); p = setDefaultConstraints(p);

The objective of the minimum variance problem is to find the weights (properties of the total investment) allocated to each asset in the portfolio that result in the lowest possible risk.

threshold = 0.1*ones(p.NumAssets,1); threshold(strcmpi('IBM',p.AssetList)) = 0.15; p = setConditionalBudget(p,threshold,0.4); % Solve the minimum risk problem wMin = estimateFrontierLimits(p,'min'); figure bar(Assets(1:12),wMin); hold on yline(0.1,'--',LineWidth=2) yline(0.15,':',LineWidth=2) title('Minimum Risk Portfolio') ylabel('Weight')

All assets except IBM and MSFT do not exceed the 10% threshold, IBM does not exceed the 15% threshold, and the sum of all the assets above their conditional threshold (in this case only MSFT) is less than 40%.

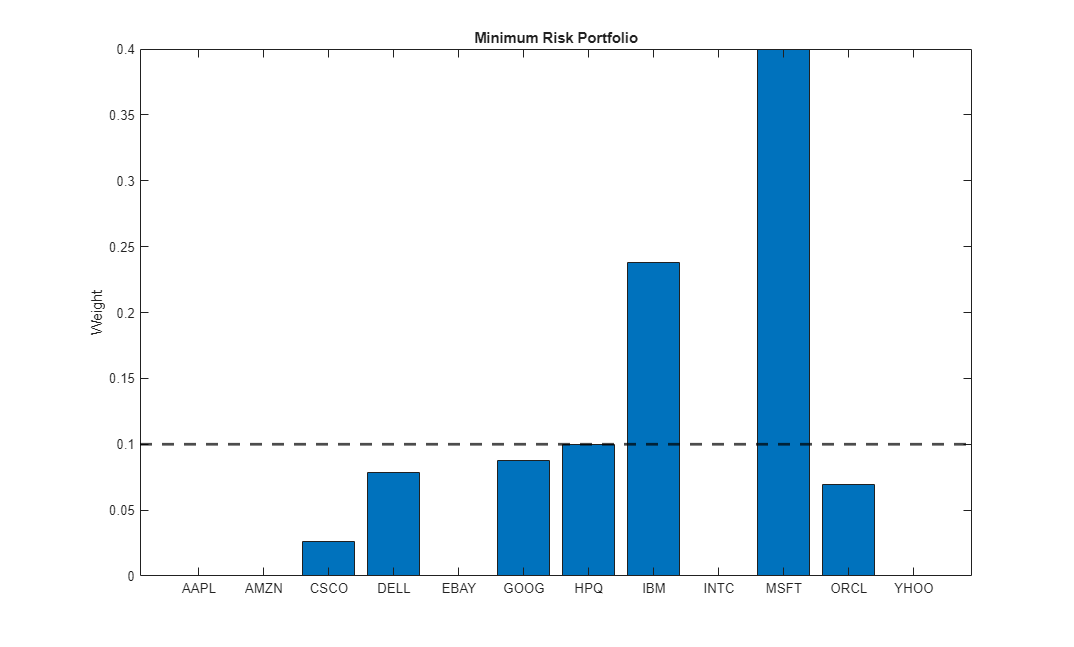

This example shows how to exclude individual assets from the conditional budget constraint.

Create a PortfolioMAD object. In addition to using a PortfolioMAD object, you can also perform this workflow using a Portfolio or PortfolioCVaR object.

% Load data load CAPMuniverse.mat tol = 1e-8; % Create a PortfolioMAD object with default constraints startRow = find(~isnan(Data(:,6)),1); q = PortfolioMAD(AssetList=Assets(1:12), ... AssetScenarios=Data(startRow:end,1:12)); % Nonnegative and fully invested portfolios q = setDefaultConstraints(q);

To exclude any asset from the conditional budget constraint, set the ConditionalBudgetThreshold of that asset to Inf. In this example, you can exclude IBM from the conditional budget constraint.

% Conditional budget threshold = 0.1*ones(q.NumAssets,1); threshold(strcmpi('IBM',q.AssetList)) = Inf; q2 = setConditionalBudget(q,threshold,0.4); % Solve minimum risk problem wMin2 = estimateFrontierLimits(q2,'min'); figure bar(Assets(1:12),wMin2); hold on yline(0.1,'--',LineWidth=2) title('Minimum Risk Portfolio') ylabel('Weight')

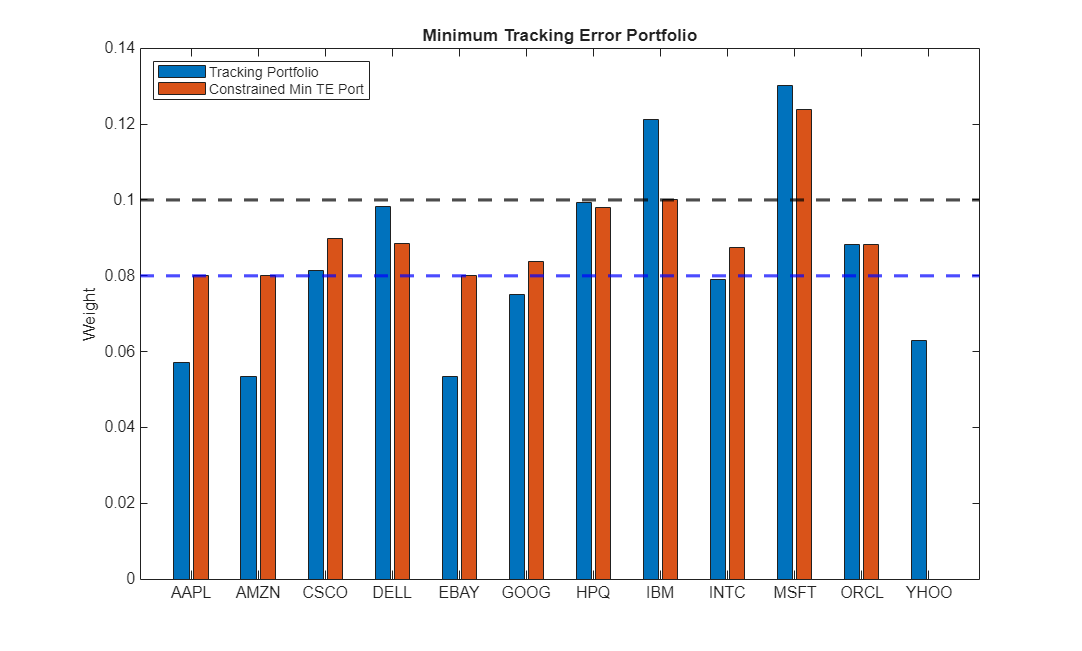

This example shows how to combine the conditional budget constraint with other types of constraints. Specifically, the example shows how to add semicontinuous bounds on the assets together with a conditional budget constraint, while ensuring that the portfolio is fully invested.

Create a mean-variance Portfolio object with default constraints.

% Load data load CAPMuniverse.mat tol = 1e-8; p = Portfolio('AssetList',Assets(1:12)); p = estimateAssetMoments(p,Data(:,1:12));

Use setBounds to ensure that any asset that is chosen in the portfolio has a weight of at least 8% and at most 15%. Then, use setBudget to set the fully invested constraint.

% Assets must be either 0 or between 8% and 15% p = setBounds(p,0.08,0.15,BoundType="conditional"); % Assets must sum to 1 p = setBudget(p,1,1); % Conditional budget p = setConditionalBudget(p,0.1,0.2);

To find the minimum tracking error portfolio that satisfies all the previously specified constraints, use the risk parity portfolio as the benchmark portfolio.

% Solve minimum tracking error portfolio trackingPort = riskBudgetingPortfolio(p.AssetCovar); TE = @(w) (w-trackingPort)'*p.AssetCovar*(w-trackingPort); wTE = estimateCustomObjectivePortfolio(p,TE); figure bar(Assets(1:12),[trackingPort wTE]); hold on yline(0.1,'--',LineWidth=2) yline(0.08,':',LineWidth=2) title('Minimum Tracking Error Portfolio') ylabel('Weight') legend('Tracking Portfolio','Constrained Min TE Port', ... Location='northwest')

All assets for the constrained portfolio are either zero or have at least a 0.08 weight, which means that the semicontinuous bound is satisfied. Furthermore, the sum of the assets above the 0.1 threshold is less than 0.2, and this result is also consistent with the conditional budget.

Input Arguments

Output Arguments

More About

Tips

You can also use dot notation to set up the conditional budget constraints.

obj = obj.setConditionalBudget(ConditionalBudgetThreshold,ConditionalUpperBudget);

Version History

Introduced in R2024b

See Also

Topics

- Adding Constraints to Satisfy UCITS Directive

- Conditional Budget Constraints

- Conditional Budget Constraints

- Conditional Budget Constraints

- Supported Constraints for Portfolio Optimization Using Portfolio Objects

- Supported Constraints for Portfolio Optimization Using PortfolioCVaR Object

- Supported Constraints for Portfolio Optimization Using PortfolioMAD Object