gjr

GJR conditional variance time series model

Description

Use gjr to specify a univariate GJR (Glosten, Jagannathan, and Runkle) model. The gjr function returns a gjr object specifying the functional form of a GJR(P,Q) model, and stores its parameter values.

The key components of a gjr model include the:

GARCH polynomial, which is composed of lagged conditional variances. The degree is denoted by P.

ARCH polynomial, which is composed of the lagged squared innovations.

Leverage polynomial, which is composed of lagged squared, negative innovations.

Maximum of the ARCH and leverage polynomial degrees, denoted by Q.

P is the maximum nonzero lag in the GARCH polynomial, and Q is the maximum nonzero lag in the ARCH and leverage polynomials. Other model components include an innovation mean model offset, a conditional variance model constant, and the innovations distribution.

All coefficients are unknown (NaN values) and estimable unless you specify their values using name-value pair argument syntax. To estimate models containing all or partially unknown parameter values given data, use estimate. For completely specified models (models in which all parameter values are known), simulate or forecast responses using simulate or forecast, respectively.

Creation

Description

Mdl = gjrgjr object.

Mdl = gjr(P,Q)Mdl) with a GARCH polynomial with a degree of P and ARCH and leverage polynomials each with a degree of Q. All polynomials contain all consecutive lags from 1 through their degrees, and all coefficients are NaN values.

This shorthand syntax enables you to create a template in which you specify the polynomial degrees explicitly. The model template is suited for unrestricted parameter estimation, that is, estimation without any parameter equality constraints. However, after you create a model, you can alter property values using dot notation.

Mdl = gjr(Name,Value)'ARCHLags',[1 4],'ARCH',{0.2 0.3} specifies the two ARCH coefficients in ARCH at lags 1 and 4.

This longhand syntax enables you to create more flexible models.

Input Arguments

Name-Value Arguments

Properties

Object Functions

estimate | Fit conditional variance model to data |

filter | Filter disturbances through conditional variance model |

forecast | Forecast conditional variances from conditional variance models |

infer | Infer conditional variances of conditional variance models |

simulate | Monte Carlo simulation of conditional variance models |

summarize | Display estimation results of conditional variance model |

Examples

Create a default gjr model object and specify its parameter values using dot notation.

Create a GJR(0,0) model.

Mdl = gjr

Mdl =

gjr with properties:

Description: "GJR(0,0) Conditional Variance Model (Gaussian Distribution)"

SeriesName: "Y"

Distribution: Name = "Gaussian"

P: 0

Q: 0

Constant: NaN

GARCH: {}

ARCH: {}

Leverage: {}

Offset: 0

Mdl is a gjr model object. It contains an unknown constant, its offset is 0, and the innovation distribution is 'Gaussian'. The model does not have GARCH, ARCH, or leverage polynomials.

Specify two unknown ARCH and leverage coefficients for lags one and two using dot notation.

Mdl.ARCH = {NaN NaN};

Mdl.Leverage = {NaN NaN};

MdlMdl =

gjr with properties:

Description: "GJR(0,2) Conditional Variance Model (Gaussian Distribution)"

SeriesName: "Y"

Distribution: Name = "Gaussian"

P: 0

Q: 2

Constant: NaN

GARCH: {}

ARCH: {NaN NaN} at lags [1 2]

Leverage: {NaN NaN} at lags [1 2]

Offset: 0

The Q, ARCH, and Leverage properties update to 2, {NaN NaN}, and {NaN NaN}, respectively. The two ARCH and leverage coefficients are associated with lags 1 and 2.

Create a gjr model object using the shorthand notation gjr(P,Q), where P is the degree of the GARCH polynomial and Q is the degree of the ARCH and leverage polynomials.

Create an GJR(3,2) model.

Mdl = gjr(3,2)

Mdl =

gjr with properties:

Description: "GJR(3,2) Conditional Variance Model (Gaussian Distribution)"

SeriesName: "Y"

Distribution: Name = "Gaussian"

P: 3

Q: 2

Constant: NaN

GARCH: {NaN NaN NaN} at lags [1 2 3]

ARCH: {NaN NaN} at lags [1 2]

Leverage: {NaN NaN} at lags [1 2]

Offset: 0

Mdl is a gjr model object. All properties of Mdl, except P, Q, and Distribution, are NaN values. By default, the software:

Includes a conditional variance model constant

Excludes a conditional mean model offset (i.e., the offset is

0)Includes all lag terms in the GARCH polynomial up to lags

PIncludes all lag terms in the ARCH and leverage polynomials up to lag

Q

Mdl specifies only the functional form of a GJR model. Because it contains unknown parameter values, you can pass Mdl and time-series data to estimate to estimate the parameters.

Create a gjr model using name-value pair arguments.

Specify a GJR(1,1) model.

Mdl = gjr('GARCHLags',1,'ARCHLags',1,'LeverageLags',1)

Mdl =

gjr with properties:

Description: "GJR(1,1) Conditional Variance Model (Gaussian Distribution)"

SeriesName: "Y"

Distribution: Name = "Gaussian"

P: 1

Q: 1

Constant: NaN

GARCH: {NaN} at lag [1]

ARCH: {NaN} at lag [1]

Leverage: {NaN} at lag [1]

Offset: 0

Mdl is a gjr model object. The software sets all parameters to NaN, except P, Q, Distribution, and Offset (which is 0 by default).

Since Mdl contains NaN values, Mdl is only appropriate for estimation only. Pass Mdl and time-series data to estimate.

Create a GJR(1,1) model with mean offset

where

and is an independent and identically distributed standard Gaussian process.

Mdl = gjr('Constant',0.0001,'GARCH',0.35,... 'ARCH',0.1,'Offset',0.5,'Leverage',{0.03 0 0.01})

Mdl =

gjr with properties:

Description: "GJR(1,3) Conditional Variance Model with Offset (Gaussian Distribution)"

SeriesName: "Y"

Distribution: Name = "Gaussian"

P: 1

Q: 3

Constant: 0.0001

GARCH: {0.35} at lag [1]

ARCH: {0.1} at lag [1]

Leverage: {0.03 0.01} at lags [1 3]

Offset: 0.5

gjr assigns default values to any properties you do not specify with name-value pair arguments. An alternative way to specify the leverage component is 'Leverage',{0.03 0.01},'LeverageLags',[1 3].

Access the properties of a gjr model object using dot notation.

Create a gjr model object.

Mdl = gjr(3,2)

Mdl =

gjr with properties:

Description: "GJR(3,2) Conditional Variance Model (Gaussian Distribution)"

SeriesName: "Y"

Distribution: Name = "Gaussian"

P: 3

Q: 2

Constant: NaN

GARCH: {NaN NaN NaN} at lags [1 2 3]

ARCH: {NaN NaN} at lags [1 2]

Leverage: {NaN NaN} at lags [1 2]

Offset: 0

Remove the second GARCH term from the model. That is, specify that the GARCH coefficient of the second lagged conditional variance is 0.

Mdl.GARCH{2} = 0Mdl =

gjr with properties:

Description: "GJR(3,2) Conditional Variance Model (Gaussian Distribution)"

SeriesName: "Y"

Distribution: Name = "Gaussian"

P: 3

Q: 2

Constant: NaN

GARCH: {NaN NaN} at lags [1 3]

ARCH: {NaN NaN} at lags [1 2]

Leverage: {NaN NaN} at lags [1 2]

Offset: 0

The GARCH polynomial has two unknown parameters corresponding to lags 1 and 3.

Display the distribution of the disturbances.

Mdl.Distribution

ans = struct with fields:

Name: "Gaussian"

The disturbances are Gaussian with mean 0 and variance 1.

Specify that the underlying disturbances have a t distribution with five degrees of freedom.

Mdl.Distribution = struct('Name','t','DoF',5)

Mdl =

gjr with properties:

Description: "GJR(3,2) Conditional Variance Model (t Distribution)"

SeriesName: "Y"

Distribution: Name = "t", DoF = 5

P: 3

Q: 2

Constant: NaN

GARCH: {NaN NaN} at lags [1 3]

ARCH: {NaN NaN} at lags [1 2]

Leverage: {NaN NaN} at lags [1 2]

Offset: 0

Specify that the ARCH coefficients are 0.2 for the first lag and 0.1 for the second lag.

Mdl.ARCH = {0.2 0.1}Mdl =

gjr with properties:

Description: "GJR(3,2) Conditional Variance Model (t Distribution)"

SeriesName: "Y"

Distribution: Name = "t", DoF = 5

P: 3

Q: 2

Constant: NaN

GARCH: {NaN NaN} at lags [1 3]

ARCH: {0.2 0.1} at lags [1 2]

Leverage: {NaN NaN} at lags [1 2]

Offset: 0

To estimate the remaining parameters, you can pass Mdl and your data to estimate and use the specified parameters as equality constraints. Or, you can specify the rest of the parameter values, and then simulate or forecast conditional variances from the GARCH model by passing the fully specified model to simulate or forecast, respectively.

Fit a GJR model to an annual time series of stock price index returns from 1861-1970.

Load the Nelson-Plosser data set. Convert the yearly stock price indices (SP) to returns. Plot the returns.

load Data_NelsonPlosser; sp = price2ret(DataTable.SP); figure; plot(dates(2:end),sp); hold on; plot([dates(2) dates(end)],[0 0],'r:'); % Plot y = 0 hold off; title('Returns'); ylabel('Return (%)'); xlabel('Year'); axis tight;

The return series does not seem to have a conditional mean offset, and seems to exhibit volatility clustering. That is, the variability is smaller for earlier years than it is for later years. For this example, assume that an GJR(1,1) model is appropriate for this series.

Create a GJR(1,1) model. The conditional mean offset is zero by default. The software includes a conditional variance model constant by default.

Mdl = gjr('GARCHLags',1,'ARCHLags',1,'LeverageLags',1);

Fit the GJR(1,1) model to the data.

EstMdl = estimate(Mdl,sp);

GJR(1,1) Conditional Variance Model (Gaussian Distribution):

Value StandardError TStatistic PValue

_________ _____________ __________ ________

Constant 0.0045728 0.0044199 1.0346 0.30086

GARCH{1} 0.55808 0.24 2.3253 0.020057

ARCH{1} 0.20461 0.17886 1.144 0.25263

Leverage{1} 0.18066 0.26802 0.67406 0.50027

EstMdl is a fully specified gjr model object. That is, it does not contain NaN values. You can assess the adequacy of the model by generating residuals using infer, and then analyzing them.

To simulate conditional variances or responses, pass EstMdl to simulate.

To forecast innovations, pass EstMdl to forecast.

Simulate conditional variance or response paths from a fully specified gjr model object. That is, simulate from an estimated gjr model or a known gjr model in which you specify all parameter values.

Load the Nelson-Plosser data set. Convert the yearly stock price indices to returns.

load Data_NelsonPlosser;

sp = price2ret(DataTable.SP);Create a GJR(1,1) model. Fit the model to the return series.

Mdl = gjr(1,1); EstMdl = estimate(Mdl,sp);

GJR(1,1) Conditional Variance Model (Gaussian Distribution):

Value StandardError TStatistic PValue

_________ _____________ __________ ________

Constant 0.0045728 0.0044199 1.0346 0.30086

GARCH{1} 0.55808 0.24 2.3253 0.020057

ARCH{1} 0.20461 0.17886 1.144 0.25263

Leverage{1} 0.18066 0.26802 0.67406 0.50027

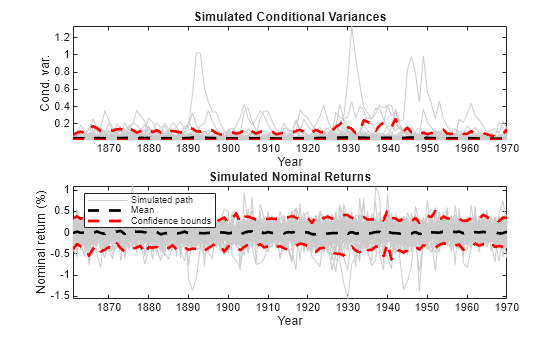

Simulate 100 paths of conditional variances and responses from the estimated GJR model.

numObs = numel(sp); % Sample size (T) numPaths = 100; % Number of paths to simulate rng(1); % For reproducibility [VSim,YSim] = simulate(EstMdl,numObs,'NumPaths',numPaths);

VSim and YSim are T-by- numPaths matrices. Rows correspond to a sample period, and columns correspond to a simulated path.

Plot the average and the 97.5% and 2.5% percentiles of the simulated paths. Compare the simulation statistics to the original data.

dates = dates(2:end); VSimBar = mean(VSim,2); VSimCI = quantile(VSim,[0.025 0.975],2); YSimBar = mean(YSim,2); YSimCI = quantile(YSim,[0.025 0.975],2); figure; subplot(2,1,1); h1 = plot(dates,VSim,'Color',0.8*ones(1,3)); hold on; h2 = plot(dates,VSimBar,'k--','LineWidth',2); h3 = plot(dates,VSimCI,'r--','LineWidth',2); hold off; title('Simulated Conditional Variances'); ylabel('Cond. var.'); xlabel('Year'); axis tight; subplot(2,1,2); h1 = plot(dates,YSim,'Color',0.8*ones(1,3)); hold on; h2 = plot(dates,YSimBar,'k--','LineWidth',2); h3 = plot(dates,YSimCI,'r--','LineWidth',2); hold off; title('Simulated Nominal Returns'); ylabel('Nominal return (%)'); xlabel('Year'); axis tight; legend([h1(1) h2 h3(1)],{'Simulated path' 'Mean' 'Confidence bounds'},... 'FontSize',7,'Location','NorthWest');

Forecast conditional variances from a fully specified gjr model object. That is, forecast from an estimated gjr model or a known gjr model in which you specify all parameter values.

Load the Nelson-Plosser data set. Convert the yearly stock price indices (SP) to returns.

load Data_NelsonPlosser;

sp = price2ret(DataTable.SP);Create a GJR(1,1) model and fit it to the return series.

Mdl = gjr('GARCHLags',1,'ARCHLags',1,'LeverageLags',1); EstMdl = estimate(Mdl,sp);

GJR(1,1) Conditional Variance Model (Gaussian Distribution):

Value StandardError TStatistic PValue

_________ _____________ __________ ________

Constant 0.0045728 0.0044199 1.0346 0.30086

GARCH{1} 0.55808 0.24 2.3253 0.020057

ARCH{1} 0.20461 0.17886 1.144 0.25263

Leverage{1} 0.18066 0.26802 0.67406 0.50027

Forecast the conditional variance of the nominal return series 10 years into the future using the estimated GJR model. Specify the entire return series as presample observations. The software infers presample conditional variances using the presample observations and the model.

numPeriods = 10; vF = forecast(EstMdl,numPeriods,sp);

Plot the forecasted conditional variances of the nominal returns. Compare the forecasts to the observed conditional variances.

v = infer(EstMdl,sp); nV = size(v,1); dates = dates((end - nV + 1):end); figure; plot(dates,v,'k:','LineWidth',2); hold on; plot(dates(end):dates(end) + 10,[v(end);vF],'r','LineWidth',2); title('Forecasted Conditional Variances of Returns'); ylabel('Conditional variances'); xlabel('Year'); axis tight; legend({'Estimation Sample Cond. Var.','Forecasted Cond. var.'},... 'Location','NorthWest');

More About

Tips

You can specify a gjr model as part of a composition of conditional mean and variance models. For details, see arima.

References

[1] Glosten, L. R., R. Jagannathan, and D. E. Runkle. “On the Relation between the Expected Value and the Volatility of the Nominal Excess Return on Stocks.” The Journal of Finance. Vol. 48, No. 5, 1993, pp. 1779–1801.

[2] Tsay, R. S. Analysis of Financial Time Series. 3rd ed. Hoboken, NJ: John Wiley & Sons, Inc., 2010.