saccr

Description

Create a saccr object using this workflow:

Create a SA-CCR CRIF file.

The ISDA® SA-CCR Common Risk Interchange Format (CRIF) is a standardized format developed by the International Swaps and Derivatives Association (ISDA) for reporting counterparty credit risk exposures under the Standardized Approach for Counterparty Credit Risk (SA-CCR) framework. For more information on creating an ISDA SA-CCR CRIF file, see ISDA SA-CCR CRIF File Specifications. SA-CCR functionality meets ISDA benchmarks for use in the

saccrobject.Create a

saccrobjectUse

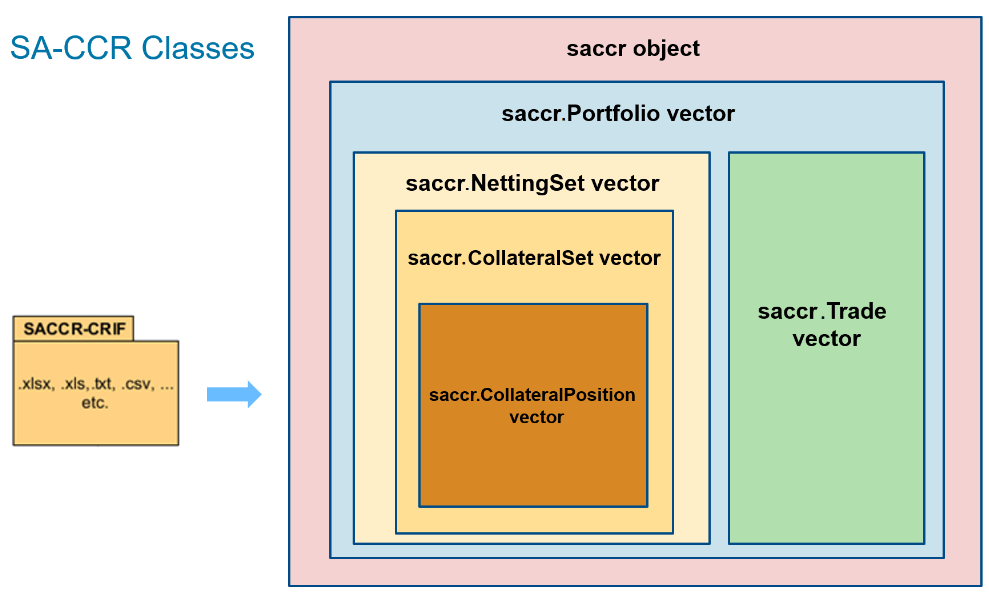

saccrto create asaccrobject. The following objects are contained in thesaccrobject:Portfolio,NettingSet,CollateralSet,CollateralPosition, andTrade. For more information, see saccr Object Structure and SA-CCR Transactional Elements.Use

saccrobject functions.Use the following functions to calculate replacement cost (RC), add-ons, potential future exposure (PFE), and exposure at default (EAD):

Aggregate EADs.

After using

addOnandead, you can useaggregateto aggregate add-ons over all asset classes or EADs over all portfolios.After using

ead, you can use theaggregateByCounterpartyto aggregate EADs by counterparty.

For more information on this workflow and a list of examples, see SA-CCR Transactional Elements and Framework for Standardized Approach to Calculating Counterparty Credit Risk: Introduction.

Creation

Description

mySACCR = saccr(SACCRCRIF)saccr object and sets the properties. The

saccr object provides an object-based framework that

supports Basel-compliant, International Swaps and Derivatives Association

(ISDA) workflows for calculating the capital banks must hold to

cover the risk that a derivative's trading partner will fail to pay its

obligation.

mySACCR = saccr(___,Name=Value)mySACCR =

saccr("SACCR_CRIF.xlsx",Alpha=1.3,DomesticCurrency="EUR",MaturityBusinessDaysFloor=7,NumBusinessDaysYear=255)

creates a saccr object. You can specify multiple

name-value arguments.

Input Arguments

Properties

Object Functions

Examples

More About

saccr Object Structure

The saccr object contains classes for Portfolio, NettingSet, CollateralSet,

CollateralPosition, and Trade.

In this framework, the following terminology applies:

Portfolio — A portfolio is a collection of derivative contracts with the same counterparty, covered by legally enforceable netting agreements. These contracts, which can vary from interest rate to credit derivatives, are managed collectively to calculate counterparty credit risk. The portfolio's defining feature is its ability to offset exposures and reduce credit risk through its netting agreements.

Netting — Netting is the process of offsetting exposures to reduce credit risk through legally enforceable agreements, consolidating derivative contracts within a portfolio for net-based credit risk calculation. It provides a more accurate counterparty credit risk assessment and reduces capital requirements by recognizing risk-reducing benefits. SA-CCR has two types of netting:

Close-Out Netting — A legal agreement allowing offsetting of positive and negative exposures upon default or termination, resulting in a single net exposure.

Collateral Netting — The use of collateral to offset exposures and reduce credit risk, considered when calculating net exposure.

Collateral — Collateral is an asset, like cash or securities, pledged by a counterparty in derivative transactions to mitigate credit risk and protect against potential losses. It serves two main purposes:

Risk Mitigation — Collateral acts as a buffer against potential losses during default or termination of contracts, reducing credit risk.

Netting and Exposure Calculation — Collateral is considered when calculating net exposure and credit risk under SA-CCR, reducing capital requirements. The eligible collateral value, typically subject to haircuts for potential market volatility or liquidity risks, is considered a reduction in exposure.

Collateral Position — A collateral position represents the status, value, and quality of the collateral involved in derivative transactions, playing a crucial role in determining credit risk mitigation and exposure calculation under SA-CCR. It assesses potential loss absorbency and risk reduction provided by the collateral, influencing net exposure and capital requirements. Key aspects in SA-CCR include:

Collateral Value — The aggregate market value of the held collateral, which can include various eligible instruments.

Haircuts — Percentage reductions applied to collateral value to account for potential market volatility or liquidity risks.

Eligibility Criteria — Requirements that collateral must meet to be considered under SA-CCR, such as liquidity and reliable valuation.

Collateral Agreements — Contractual terms outlining rights and obligations related to collateral posting, maintenance, and release.

Margining — Margining is the process of requiring collateral to cover potential losses in derivative transactions, reducing counterparty credit risk and lowering SA-CCR exposure and capital requirements. Key concepts include:

Initial Margin — The upfront collateral required at the start of a derivative transaction, serving as a buffer against losses.

Variation Margin — Regularly adjusted collateral reflecting the current market value of the positions.

Margin Calls — Requests for additional collateral triggered by changes in market prices or risk factors.

Collateral Rehypothecation — The re-use of posted collateral by the receiving party, subject to conditions and agreements, providing protection to the posting party.

Trade — A trade is a single derivative transaction between two counterparties, used as a unit for calculating counterparty credit risk and capital requirements. Under SA-CCR, each trade is individually evaluated based on its risk profile, underlying assets, and terms. Trades are grouped into portfolios based on the counterparty and netting agreements for aggregation and risk offset consideration. The SA-CCR framework considers factors like notional amount, market value, remaining maturity, risk factors, and add-on factors for each trade. This detailed analysis, considering both individual trades and portfolio netting benefits, provides a comprehensive assessment of counterparty credit risk, helping to determine capital requirements to cover potential losses.

For more information on the elements of the SA-CCR regulatory framework, see SA-CCR Transactional Elements.

References

[1] Bank for International Settlements. "CRE52 - Standardised Approach to Counterparty Credit Risk." June 2020. Available at: https://www.bis.org/basel_framework/chapter/CRE/52.htm.

[2] Bank for International Settlements. "CRE51 - Counterparty Credit Risk Overview." January 2022. Available at: https://www.bis.org/basel_framework/chapter/CRE/51.htm.

[3] Bank for International Settlements. "CRE22- Standardised Approach: Credit Risk Migration." November 2020. Available at: https://www.bis.org/basel_framework/chapter/CRE/22.htm.

[4] Bank for International Settlements. "Basel Committee on Banking Supervision: The Standardised Approach for Measuring Counterparty Credit Risk Exposures." April 2014. Available at: https://www.bis.org/publ/bcbs279.pdf.

Version History

Introduced in R2024a

See Also

Functions

Topics

- Framework for Standardized Approach to Calculating Counterparty Credit Risk: Introduction

- Create saccr Object and Compute Regulatory Values for Interest-Rate Swap

- Create saccr Object and Compute Regulatory Values for Forward FX Swap

- Create saccr Object and Compute Regulatory Values for Two CDS Trades

- Create saccr Object and Compute Regulatory Values for Multiple Asset Classes

- Create saccr Object and Compute Regulatory Values for Multiple Asset Classes with Netting Set

- Create saccr Object and Compute Regulatory Values for Multiple Asset Classes with Netting Set and Collateral Set

- Create saccr Object and Compute Regulatory Values for Multiple Asset Classes with Netting Set, Collateral Set, and Collateral Positions

- Create saccr Object and Compute Regulatory Values for Multiple Portfolios Containing Multiple Asset Classes

- SA-CCR Transactional Elements

- ISDA SA-CCR CRIF File Specifications

You can also select a web site from the following list:

Americas

- América Latina (Español)

- Canada (English)

- United States (English)

Europe

- Belgium (English)

- Denmark (English)

- Deutschland (Deutsch)

- España (Español)

- Finland (English)

- France (Français)

- Ireland (English)

- Italia (Italiano)

- Luxembourg (English)

- Netherlands (English)

- Norway (English)

- Österreich (Deutsch)

- Portugal (English)

- Sweden (English)

- Switzerland

- United Kingdom (English)